Commentary: Bangladesh’s Power Sector Reform Must Start with Bifurcation

Editorial Desk :

Bangladesh does not have a power shortage. It has a power structure that no longer serves the public interest.

According to BPDB’s own installed capacity statement, the country has over 21 GW of derated installed capacity (excluding imports). Yet on 26 February 2026, the system’s probable maximum demand was only 12.5 GW.

That single day tells the story: nearly 8,000 MW of capacity was not required.

Average daily demand sits between 12 and 14 GW.

Even maximum peaks rarely exceed 18 GW. Against more than 27 GW of total capacity nationally, Bangladesh is paying for power it does not need. And it is paying dearly.

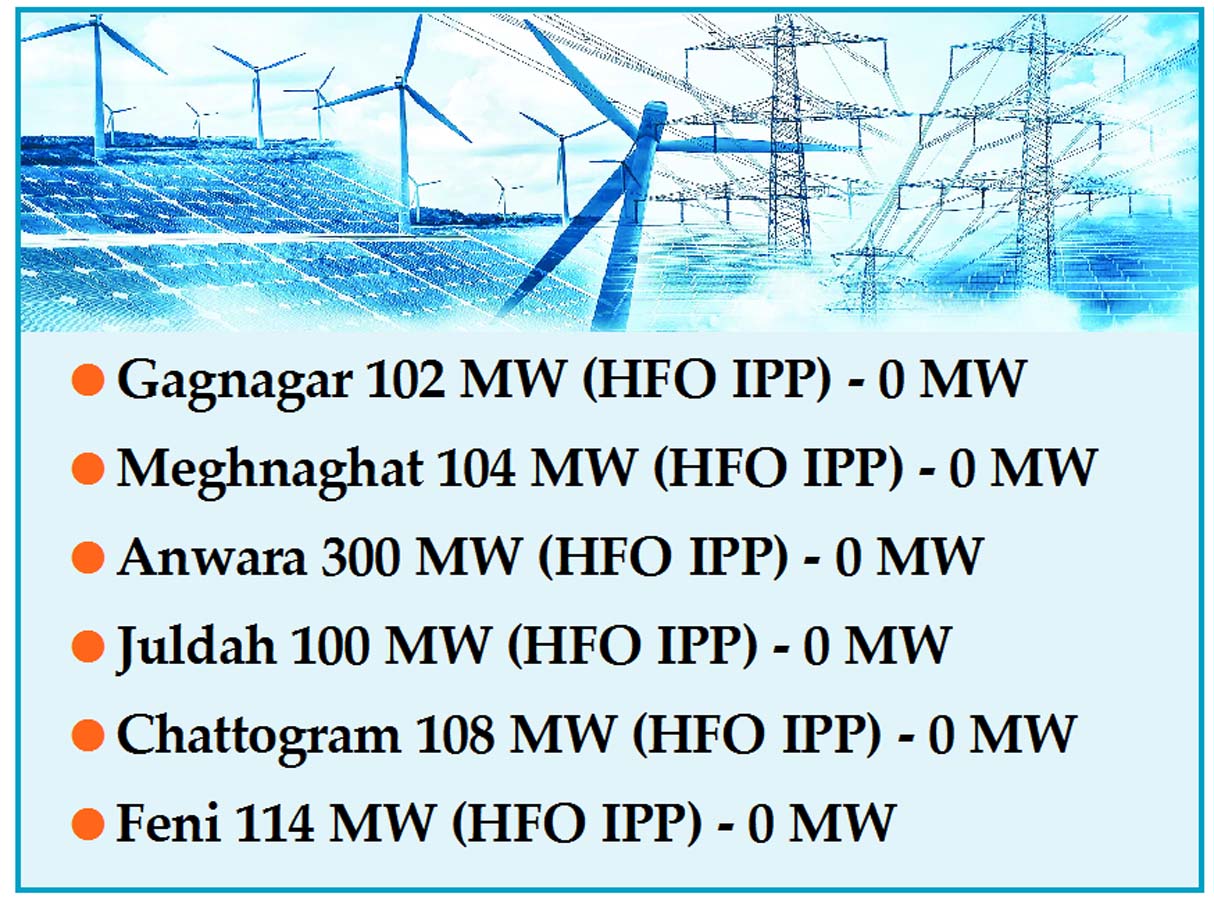

Paid to Sit Idle:

On that same day – 26 February 2026 – multiple oil-fired IPPs produced zero megawatts, including during evening peak hours.

Among them:

# Gagnagar 102 MW (HFO IPP) – 0 MW

# Meghnaghat 104 MW (HFO IPP) – 0 MW

# Anwara 300 MW (HFO IPP) – 0 MW

# Juldah 100 MW (HFO IPP) – 0 MW

# Chattogram 108 MW (HFO IPP) – 0 MW

# Feni 114 MW (HFO IPP) – 0 MW

These plants were not broken. They were simply unnecessary.

Yet they continue to receive capacity payments.

A typical 100 MW HFO-based power plant in Bangladesh receives approximately USD 1 to 1.5 million every month in capacity

payments – whether it runs or not.

That is USD 12-18 million per year for sitting idle.

Multiply that across dozens of liquid-fuel plants and the result is a structural drain on:

# BPDB finances

# The national budget

# Foreign exchange reserves

# Consumers’ electricity bills

This is not market efficiency. This is a system designed without accountability.

The Law That Must Be Revisited:

At the center of this distortion is the Quick Enhancement of Electricity and Energy Supply (Special Provisions) Act, 2010.

Roughly 65 projects were approved under this emergency law.

It was passed during a real crisis. Bangladesh needed rapid capacity.

But emergency powers became a parallel procurement universe.

Contracts were awarded without competitive price discovery. Tariffs were locked in. Capacity charges were guaranteed.

And now, long after the crisis has passed, those contracts continue to shape the sector.

Reform cannot begin without a clear bifurcation:

1. Projects won through open competitive tender.

2. Projects awarded under emergency special provisions.

Treating them as identical is intellectually dishonest and fiscally reckless.

The Fuel Question No One Wants to Ask:

There is another structural weakness – and it lies in fuel imports. Most liquid-fuel power plants are allowed to import fuel directly.

That means:

# Dozens of separate international fuel contracts.

# Fragmented procurement instead of bulk purchasing.

# Direct foreign exchange outflows from multiple private entities.

In a country under recurring forex pressure, this structure is economically irrational.

Even more concerning is the incentive problem.

Fuel costs are tied to declared plant efficiency and heat rates. If efficiency benchmarks are weakly enforced or not independently audited, excess fuel consumption translates directly into higher dollar outflows.

This is not merely a technical matter. It is a macroeconomic vulnerability.

The government has a simple option:

Require all liquid-fuel power plants to procure fuel through Bangladesh Petroleum Corporation (BPC).

With centralized procurement:

# The government can purchase in bulk through international tenders.

# Unit prices fall through scale.

# Foreign exchange outflows are consolidated and transparent.

# Fuel allocation can be audited against actual generation and heat rates.

Instead of dozens of fragmented imports, there would be a single coordinated strategy.

The Secondary Market Reality:

Anyone familiar with the Chattogram port area knows that petroleum logistics are not a small operation. When large volumes of fuel move through decentralized channels, secondary trading and reallocation risks increase.

If Bangladesh is serious about protecting foreign exchange and ensuring fuel discipline, it must bring liquid fuel procurement under tighter centralized control.

This is not anti-private sector. It is pro-national interest.

A Reform Roadmap:

The reform agenda is straightforward:

1. Full Transparency

Publish the complete list of projects awarded under the 2010 Special Provisions Act.

Tag them clearly in daily generation reports.

Let the public see which plants are idle – and still being paid.

2. Tariff Harmonization

Align tariffs of non-competitive projects with benchmarks established through competitive tenders by fuel type.

No premium for bypassing competition.

3. Centralized Fuel Procurement

Mandate that liquid-fuel plants procure through BPC, leveraging volume and enforcing efficiency audits.

From Shortage to Capture:

The 2010 law solved a shortage.

But it also created a system vulnerable to political favoritism, fiscal leakage, and opacity.

Bangladesh today does not face darkness from power cuts.

It faces a different danger – a power sector financially structured in ways that reward excess, protect non-competitive contracts, and drain scarce foreign exchange.

The crisis of shortage has ended.

The crisis of structure remains.

If reform is serious, it must begin where it is hardest:

Separate the contracts. Standardize the tariffs. Centralize fuel procurement. Publish the data.

Only then can Bangladesh claim that its power sector serves the people – not the privileged.